Attorney-Verified California Deed in Lieu of Foreclosure Template

Documents PDF

Attorney-Verified California Deed in Lieu of Foreclosure Template

The California Deed in Lieu of Foreclosure form serves as an important option for homeowners facing financial difficulties and potential foreclosure. This legal document allows a homeowner to voluntarily transfer ownership of their property to the lender in exchange for the cancellation of their mortgage debt. By choosing this route, homeowners can avoid the lengthy and often stressful foreclosure process. The form typically outlines the terms of the transfer, including the condition of the property and any outstanding debts. It also addresses the rights and responsibilities of both the homeowner and the lender during the transaction. This alternative can provide a fresh start for homeowners while enabling lenders to recover their losses more efficiently. Understanding the implications and requirements of this form is crucial for anyone considering this option in California.

After completing the California Deed in Lieu of Foreclosure form, the next steps involve submitting the document to the appropriate parties, typically the lender, and ensuring that all necessary signatures are obtained. This process may also include recording the deed with the county recorder's office to finalize the transfer of ownership.

When dealing with the California Deed in Lieu of Foreclosure, several misconceptions often arise. Understanding these can help homeowners make informed decisions about their options. Below are five common misunderstandings:

Understanding these misconceptions can empower homeowners to navigate their options more effectively and make choices that align with their financial situations.

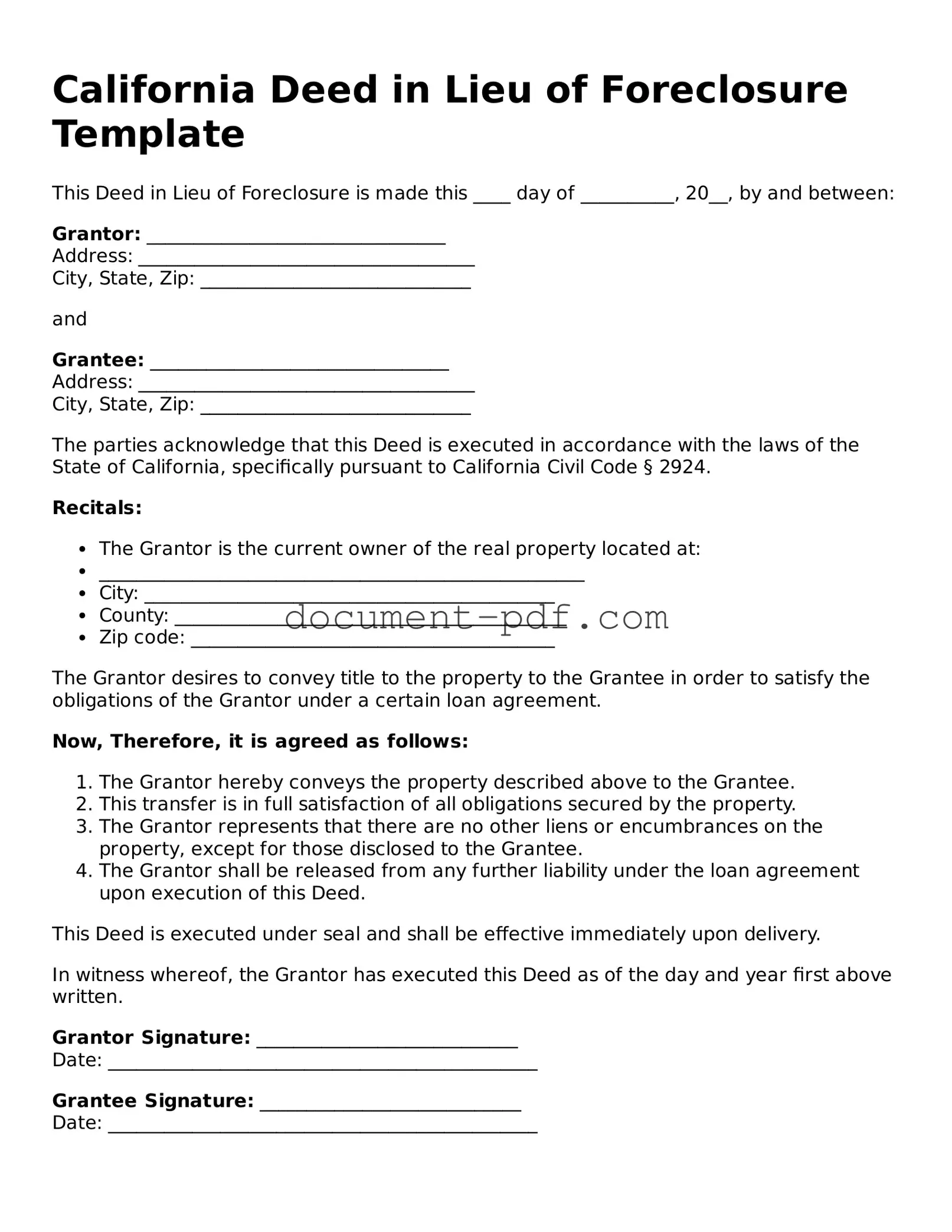

California Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure is made this ____ day of __________, 20__, by and between:

Grantor: ________________________________

Address: ____________________________________

City, State, Zip: _____________________________

and

Grantee: ________________________________

Address: ____________________________________

City, State, Zip: _____________________________

The parties acknowledge that this Deed is executed in accordance with the laws of the State of California, specifically pursuant to California Civil Code § 2924.

Recitals:

The Grantor desires to convey title to the property to the Grantee in order to satisfy the obligations of the Grantor under a certain loan agreement.

Now, Therefore, it is agreed as follows:

This Deed is executed under seal and shall be effective immediately upon delivery.

In witness whereof, the Grantor has executed this Deed as of the day and year first above written.

Grantor Signature: ____________________________

Date: ______________________________________________

Grantee Signature: ____________________________

Date: ______________________________________________

State of California

County of __________________________________________

On this ___ day of __________, 20__, before me, ________________, a Notary Public in and for said county, personally appeared ______________________, known to me to be the person whose name is subscribed to the within instrument and acknowledged that he/she executed the same.

Witness my hand and official seal.

Signature: _________________________________________

Notary Public for the State of California

When considering the California Deed in Lieu of Foreclosure form, it is essential to understand several key aspects that can impact the process. This document allows a homeowner to voluntarily transfer ownership of their property to the lender in exchange for the cancellation of the mortgage debt. Below are important takeaways to keep in mind:

By keeping these points in mind, homeowners can navigate the deed in lieu of foreclosure process more effectively, ensuring a smoother transition during a challenging time.

Deed in Lieu Vs Foreclosure - In many cases, homeowners may be able to negotiate a release from further obligations related to the mortgage debt.

For those seeking further information about the necessary documentation, the NYCERS F170 form can be obtained from sources like New York PDF Docs, ensuring that you have the right tools to navigate the retirement options available to EMT members.

Deed in Lieu of Foreclosure Sample - A tool that embodies an amicable resolution to housing financial issues.

When filling out the California Deed in Lieu of Foreclosure form, it's important to follow specific guidelines to ensure the process goes smoothly. Here’s a list of things to do and avoid:

The California Deed in Lieu of Foreclosure form is similar to a mortgage release. A mortgage release occurs when a lender agrees to release a borrower from the obligations of a mortgage. This document serves to formally acknowledge that the borrower has satisfied their debt, either through payment or another arrangement. Like a deed in lieu, it helps borrowers avoid foreclosure and allows them to move forward without the burden of an outstanding mortgage. Both documents aim to simplify the process of resolving mortgage defaults, providing a clear path for borrowers seeking relief.

Another document comparable to the Deed in Lieu of Foreclosure is a short sale agreement. In a short sale, the lender allows the homeowner to sell the property for less than the amount owed on the mortgage. The lender agrees to accept this lesser amount as full payment, which helps the homeowner avoid foreclosure. Similar to a deed in lieu, a short sale can prevent the negative consequences of foreclosure on a borrower's credit report. Both options require lender approval and can provide a more amicable resolution for distressed homeowners.

A loan modification agreement also shares similarities with the Deed in Lieu of Foreclosure. This document modifies the terms of an existing loan to make it more manageable for the borrower. It may involve lowering the interest rate, extending the loan term, or reducing the principal balance. Like a deed in lieu, a loan modification seeks to help homeowners retain their property while alleviating financial strain. Both solutions aim to prevent foreclosure, although they approach the problem from different angles.

A foreclosure settlement agreement is another document that resembles the Deed in Lieu of Foreclosure. This agreement typically occurs after a borrower has defaulted but before the foreclosure process is completed. It outlines the terms under which the borrower can settle their debt with the lender, often allowing for a payment plan or a lump sum payment. Similar to a deed in lieu, this agreement provides an alternative to foreclosure, allowing the borrower to resolve their financial issues without losing their home.

In the context of managing rental agreements, understanding legal documents like the Texas Notice to Quit is critical for both landlords and tenants. This form serves as an official notification from landlords indicating their intent to terminate a rental arrangement and provides tenants with a specific timeframe to vacate the property. For those looking for a template for this notice, you can find a free version at https://texasformsonline.com/free-notice-to-quit-template, which can help ensure compliance with state rental laws.

The forbearance agreement is yet another document that aligns with the principles of a Deed in Lieu of Foreclosure. In this arrangement, a lender agrees to temporarily suspend or reduce mortgage payments for a specified period. This can provide borrowers with the necessary time to regain their financial footing. While a deed in lieu involves transferring ownership of the property, both documents aim to help borrowers avoid the severe consequences of foreclosure by offering a temporary reprieve.

A quitclaim deed also bears resemblance to the Deed in Lieu of Foreclosure. This document allows a property owner to transfer their interest in a property to another party without any warranties. In situations where a borrower cannot afford their mortgage, they may use a quitclaim deed to transfer the property to the lender as part of a deed in lieu arrangement. Both documents facilitate the transfer of ownership and can help borrowers avoid the lengthy foreclosure process.

Lastly, a bankruptcy filing can be compared to the Deed in Lieu of Foreclosure. When individuals file for bankruptcy, they seek relief from their debts, which may include their mortgage obligations. While bankruptcy can halt foreclosure proceedings temporarily, it does not directly address the property itself. However, both options provide a means for borrowers to manage overwhelming debt and avoid the repercussions of foreclosure. Each approach offers different benefits and consequences, but both aim to assist borrowers in regaining control over their financial situations.