Attorney-Approved Deed in Lieu of Foreclosure Document

Documents PDF

Attorney-Approved Deed in Lieu of Foreclosure Document

When facing the possibility of foreclosure, homeowners may find themselves overwhelmed by options and decisions. One alternative that can provide a smoother resolution is the Deed in Lieu of Foreclosure. This process allows a homeowner to voluntarily transfer ownership of their property back to the lender, effectively settling the mortgage debt without going through the lengthy foreclosure process. By signing the Deed in Lieu of Foreclosure form, the homeowner can often avoid the negative impact of foreclosure on their credit score. This form typically includes essential details such as the property description, the names of the parties involved, and any terms related to the transfer. It serves as a formal agreement, ensuring that both the homeowner and the lender understand their rights and responsibilities. In many cases, lenders may also agree to forgive any remaining debt, making this option appealing for those who wish to move on from their financial struggles. Understanding the implications of this form can empower homeowners to make informed decisions during a challenging time.

Once you have decided to proceed with a Deed in Lieu of Foreclosure, it’s essential to fill out the form accurately. This process involves providing specific information about your property and your situation. After completing the form, you will typically submit it to your lender for review, and they will guide you through the next steps.

Many homeowners facing financial difficulties may consider a Deed in Lieu of Foreclosure as a potential solution. However, several misconceptions surround this option. Understanding these misconceptions can help individuals make informed decisions.

Understanding these misconceptions can empower homeowners to make better decisions regarding their financial situations and the potential impact of a Deed in Lieu of Foreclosure.

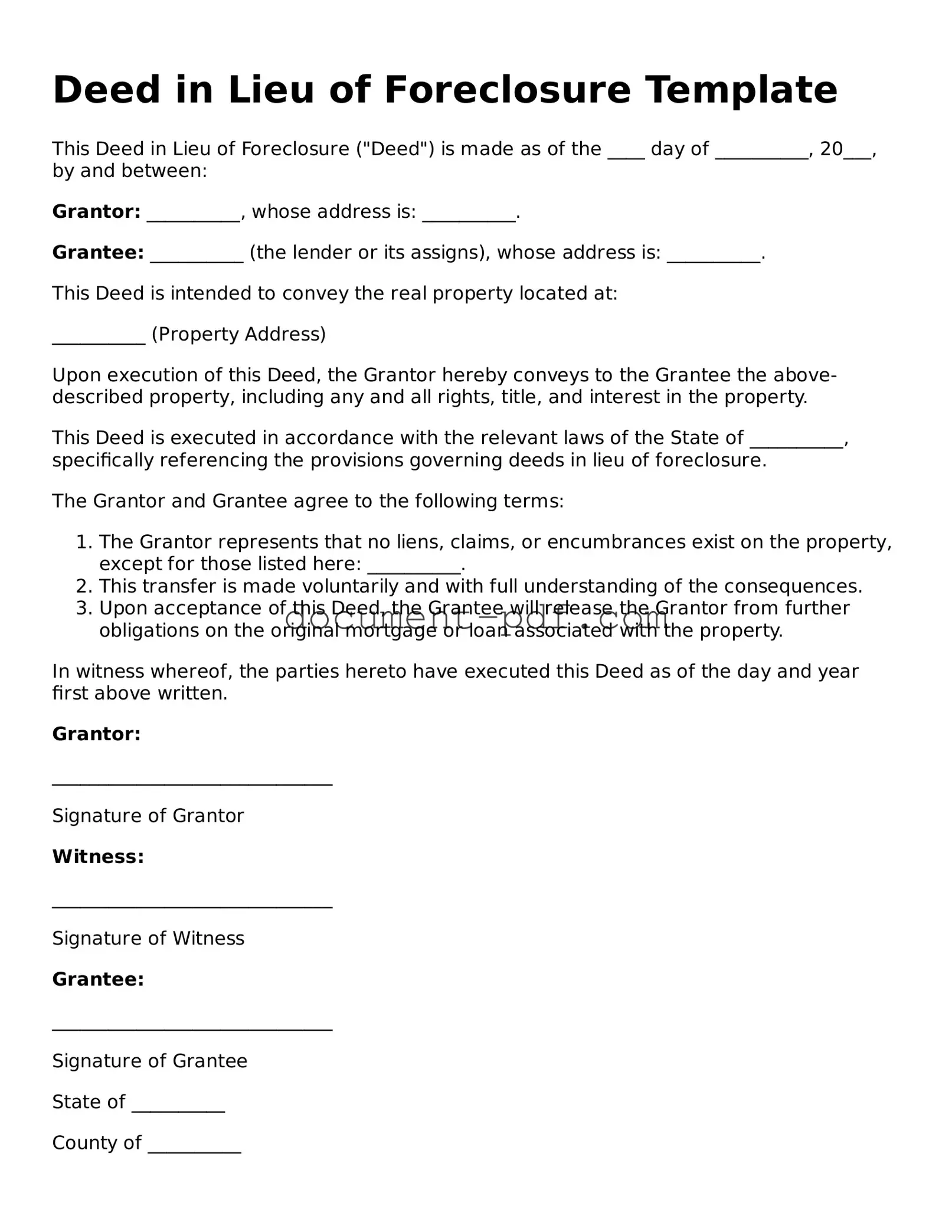

Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure ("Deed") is made as of the ____ day of __________, 20___, by and between:

Grantor: __________, whose address is: __________.

Grantee: __________ (the lender or its assigns), whose address is: __________.

This Deed is intended to convey the real property located at:

__________ (Property Address)

Upon execution of this Deed, the Grantor hereby conveys to the Grantee the above-described property, including any and all rights, title, and interest in the property.

This Deed is executed in accordance with the relevant laws of the State of __________, specifically referencing the provisions governing deeds in lieu of foreclosure.

The Grantor and Grantee agree to the following terms:

In witness whereof, the parties hereto have executed this Deed as of the day and year first above written.

Grantor:

______________________________

Signature of Grantor

Witness:

______________________________

Signature of Witness

Grantee:

______________________________

Signature of Grantee

State of __________

County of __________

On this ____ day of __________, 20___, before me, a notary public, personally appeared __________ (the Grantor) and __________ (the Grantee), known to me to be the persons whose names are subscribed to the within instrument, and acknowledged that they executed the same for the purposes therein contained.

Witness my hand and official seal:

______________________________

Notary Public

My commission expires: __________

When considering a Deed in Lieu of Foreclosure, it's essential to understand the implications and processes involved. Here are some key takeaways:

Understanding these points can help you make an informed decision about using a Deed in Lieu of Foreclosure.

Free Printable Gift Deed Form - Gift Deeds can differ in format, but must include essential elements to be valid.

When entering into a room rental situation, it is crucial for both landlords and tenants to understand the terms laid out in the New York Room Rental Agreement. This agreement not only clarifies the expectations surrounding rent and security deposits but also delineates the responsibilities of each party. For those looking for a reliable source to obtain this document, New York PDF Docs can be a valuable resource.

Quit Claim Deed Form Iowa - This deed emphasizes the relinquishment of rights rather than the promise of ownership quality.

Free Printable Michigan Lady Bird Deed Form - A Lady Bird Deed allows for a smoother transfer process with fewer legal hurdles to navigate.

When filling out the Deed in Lieu of Foreclosure form, it's important to approach the process carefully. Here are some key things to keep in mind:

A short sale is a process in which a homeowner sells their property for less than the amount owed on the mortgage. Like a deed in lieu of foreclosure, a short sale allows the homeowner to avoid the lengthy and often damaging process of foreclosure. In both cases, the lender agrees to accept less than the full amount owed, which can help the homeowner mitigate the negative impact on their credit score. However, while a deed in lieu transfers ownership directly to the lender, a short sale requires the sale of the property to a third party before the lender receives any funds.

A loan modification is another option for homeowners facing financial difficulties. This document alters the original terms of the mortgage to make payments more manageable. Similar to a deed in lieu of foreclosure, a loan modification aims to help the homeowner keep their home and avoid foreclosure. While a deed in lieu transfers ownership to the lender, a loan modification allows the homeowner to remain in their property by adjusting the payment structure, interest rate, or loan term.

For those navigating the complexities of real estate transactions, it's essential to understand the significance of proper documentation. A well-crafted purchase agreement can mitigate potential disputes by clearly defining the responsibilities and expectations of both parties involved. You can find a valuable resource to aid in this process at texasformsonline.com/free-real-estate-purchase-agreement-template, which offers templates that help ensure a smooth transaction.

Bankruptcy can serve as a legal strategy for individuals struggling with overwhelming debt, including mortgage obligations. Filing for bankruptcy may stop foreclosure proceedings temporarily, giving the homeowner time to reorganize their finances. Like a deed in lieu of foreclosure, bankruptcy can provide relief from the stress of financial burdens. However, unlike a deed in lieu, bankruptcy involves a court process and can have long-lasting effects on the individual’s credit report.

A forbearance agreement is a temporary solution that allows homeowners to pause or reduce their mortgage payments for a specified period. This document is similar to a deed in lieu of foreclosure in that both aim to provide relief to distressed homeowners. While a deed in lieu results in the transfer of the property to the lender, a forbearance agreement keeps the homeowner in their home while they regain financial stability. Once the forbearance period ends, the homeowner must resume payments, potentially with a repayment plan.

Lastly, a mortgage release is a document that formally releases a borrower from their mortgage obligation, often in exchange for a deed in lieu of foreclosure. This document is similar to a deed in lieu in that it allows the homeowner to relinquish their property without going through the foreclosure process. Both options provide a way for the homeowner to exit their mortgage agreement, but a mortgage release typically follows a deed in lieu, as it finalizes the lender's acceptance of the property in lieu of foreclosure.