Attorney-Approved Employee Loan Agreement Document

Documents PDF

Attorney-Approved Employee Loan Agreement Document

When an employer offers financial assistance to an employee, an Employee Loan Agreement form becomes an essential document to ensure clarity and protection for both parties involved. This form typically outlines the terms of the loan, including the amount borrowed, the interest rate, and the repayment schedule. It serves as a formal record, detailing the responsibilities of the employee and the employer, and helps to prevent misunderstandings that could arise during the repayment period. Key components often found in this agreement include the purpose of the loan, any collateral required, and the consequences of defaulting on the loan. By establishing these parameters, the Employee Loan Agreement not only provides a framework for the transaction but also fosters a sense of trust and accountability between the employer and employee. Understanding the intricacies of this form is crucial for both parties to navigate the financial assistance process smoothly and effectively.

Filling out the Employee Loan Agreement form is straightforward. This form is essential for documenting the terms of a loan between the employer and employee. Make sure to have all necessary information ready before you start.

Once you have completed the form, review it for accuracy. Make sure all information is correct before submitting it to your HR department or the designated loan officer.

When it comes to Employee Loan Agreements, there are several misconceptions that can lead to confusion for both employees and employers. Understanding these misconceptions can help foster a clearer dialogue and ensure that both parties are on the same page.

This is not true. While both documents involve the employer and employee, an Employee Loan Agreement specifically outlines the terms of a loan, including repayment schedules, interest rates, and consequences of default.

Many believe that there are no limits to the amount an employee can borrow. In reality, the employer typically sets a maximum loan amount based on various factors, including the employee's salary and tenure.

While some employers may offer favorable terms, this is not a universal truth. Interest rates can vary widely based on the company's policies and the specific agreement.

Many people think that these agreements are set in stone. However, modifications can be made if both parties agree to the changes and document them appropriately.

This assumption can be misleading. While there is no legal obligation to disclose, failing to do so may affect an employee's creditworthiness or financial reputation.

Some employees mistakenly believe that taking out a loan from their employer protects them from termination. Job security is typically based on performance and company policy, not on loan status.

This is a common misunderstanding. Employers often have the right to take certain actions, such as deducting loan payments from future wages, if an employee fails to repay the loan.

It is a common belief that loans from employers are not subject to taxation. In reality, if the loan is forgiven or not repaid, it may be considered taxable income.

Some employers think they can create these agreements without any legal oversight. However, failing to comply with state and federal regulations can lead to legal repercussions.

This is not always the case. Eligibility often depends on the company's policies, the employee's length of service, and other criteria set by the employer.

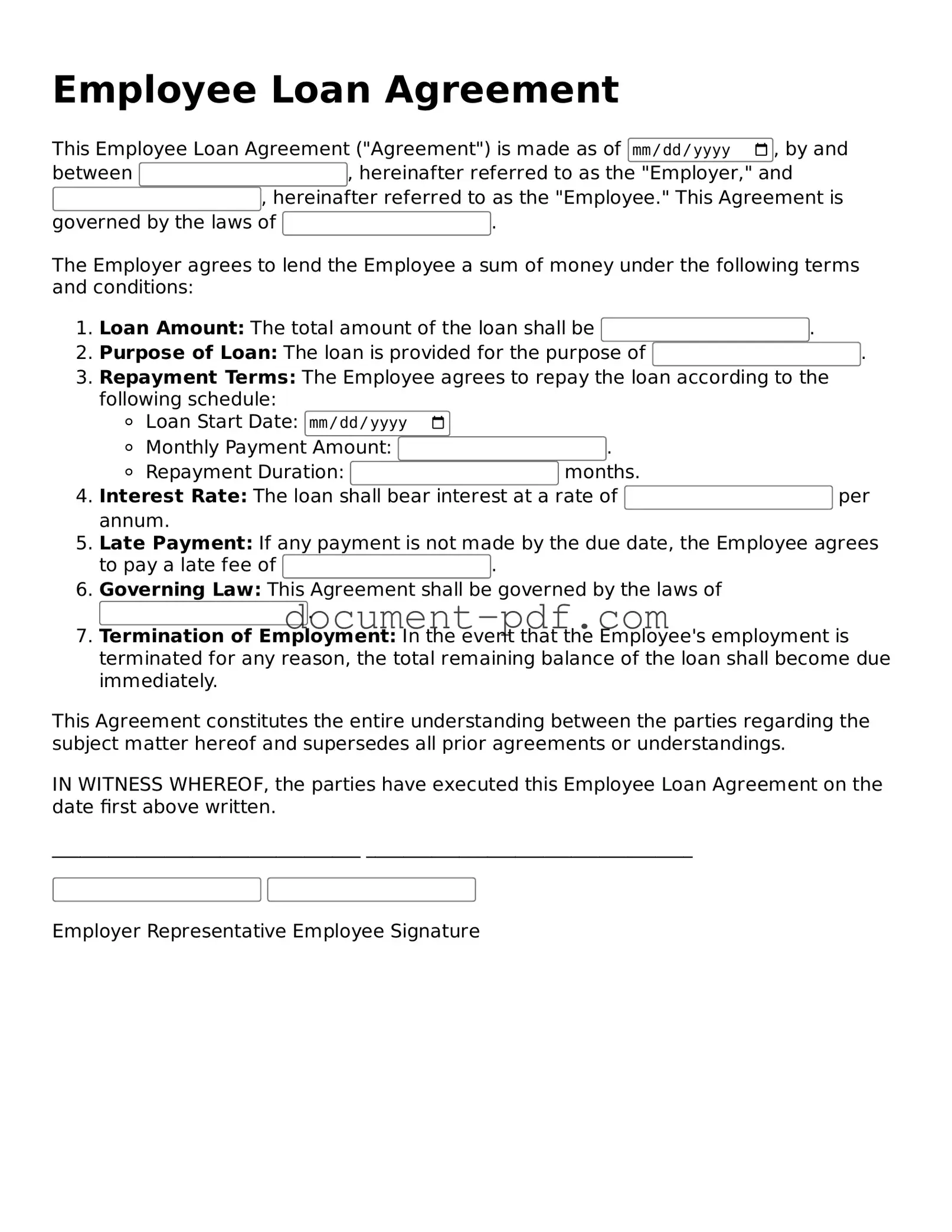

Employee Loan Agreement

This Employee Loan Agreement ("Agreement") is made as of , by and between , hereinafter referred to as the "Employer," and , hereinafter referred to as the "Employee." This Agreement is governed by the laws of .

The Employer agrees to lend the Employee a sum of money under the following terms and conditions:

This Agreement constitutes the entire understanding between the parties regarding the subject matter hereof and supersedes all prior agreements or understandings.

IN WITNESS WHEREOF, the parties have executed this Employee Loan Agreement on the date first above written.

_________________________________ ___________________________________

Employer Representative Employee Signature

Filling out and using the Employee Loan Agreement form is an important process that ensures clarity and accountability between the employer and the employee. Here are some key takeaways to keep in mind:

By keeping these key points in mind, the process of filling out and utilizing the Employee Loan Agreement can be straightforward and beneficial for both the employer and the employee.

When filling out the Employee Loan Agreement form, it is important to follow certain guidelines to ensure accuracy and compliance. Below are six recommendations on what to do and what to avoid.

The Employee Loan Agreement is quite similar to a Personal Loan Agreement. Both documents outline the terms under which one party lends money to another. In a Personal Loan Agreement, the borrower may be an individual seeking funds for various personal needs, such as medical expenses or home repairs. Like the Employee Loan Agreement, this document specifies repayment terms, interest rates, and consequences for defaulting on the loan.

Another document that shares similarities is the Promissory Note. This is a straightforward legal document where one party promises to pay a specific amount to another party. The Promissory Note typically includes details such as the loan amount, interest rate, and repayment schedule. Both the Employee Loan Agreement and the Promissory Note serve to formalize a borrowing arrangement, ensuring that both parties understand their obligations.

A Business Loan Agreement also resembles the Employee Loan Agreement. This document is used when a business borrows money from a lender, such as a bank or financial institution. Like the Employee Loan Agreement, it outlines the loan amount, interest rates, and repayment terms. However, a Business Loan Agreement often includes additional clauses related to business operations and collateral, which may not be present in an Employee Loan Agreement.

The Mortgage Agreement is another document that has a similar structure to the Employee Loan Agreement. While a Mortgage Agreement specifically pertains to real estate transactions, it also details the loan amount, interest rate, and repayment terms. Both documents aim to protect the lender's interests while ensuring the borrower understands their financial obligations.

A Lease Agreement can also be compared to an Employee Loan Agreement in terms of structure and purpose. While a Lease Agreement is primarily for renting property, it includes terms about payments, duration, and responsibilities of both parties. In both agreements, clarity on terms is crucial to prevent misunderstandings and ensure compliance.

The Credit Agreement is another document that shares characteristics with the Employee Loan Agreement. This agreement is often used in credit transactions and outlines the terms under which a lender extends credit to a borrower. Like the Employee Loan Agreement, it specifies repayment terms, interest rates, and any fees associated with the loan, making it essential for both parties to be on the same page.

An Installment Loan Agreement is similar in that it involves borrowing a specific amount of money that is paid back in installments over time. This agreement details the payment schedule, interest rate, and any penalties for late payments. Both the Employee Loan Agreement and the Installment Loan Agreement provide a clear framework for repayment, ensuring that borrowers understand their financial commitments.

The Car Loan Agreement is another document that bears resemblance to the Employee Loan Agreement. This type of agreement is used when financing the purchase of a vehicle. It includes similar elements, such as the loan amount, interest rate, and repayment terms. Both agreements aim to protect the lender while providing the borrower with the necessary funds to make a purchase.

The Employee Loan Agreement form bears similarity to the Personal Loan Agreement. In both documents, borrowers receive funds from a lender, typically a financial institution or employer, under specific terms outlined in writing. These agreements stipulate the amount borrowed, interest rates, repayment timelines, and consequences of defaulting. The focus shifts between the informal nature of personal loans and the structured environment of employment, yet the core principles of record-keeping and mutual responsibilities remain intact. For detailed templates and examples, you can refer to All Florida Forms.

The Student Loan Agreement also shares common features with the Employee Loan Agreement. This document outlines the terms under which a student borrows money for educational expenses. Like the Employee Loan Agreement, it specifies the loan amount, interest rates, and repayment terms, making it essential for students to understand their obligations after graduation.

Lastly, a Secured Loan Agreement is akin to the Employee Loan Agreement in that it involves borrowing money with collateral. This document outlines the terms of the loan, including the collateral being offered, interest rates, and repayment terms. Both agreements aim to protect the lender's interests while providing the borrower with the necessary funds, ensuring that all parties are aware of their rights and responsibilities.