Attorney-Verified Georgia Deed in Lieu of Foreclosure Template

Documents PDF

Attorney-Verified Georgia Deed in Lieu of Foreclosure Template

In the state of Georgia, homeowners facing financial difficulties may find themselves exploring various options to avoid foreclosure. One such option is the Deed in Lieu of Foreclosure, a legal process that allows a borrower to voluntarily transfer their property title back to the lender. This arrangement can serve as a practical solution, enabling homeowners to mitigate the negative impacts of foreclosure on their credit scores and financial future. By completing this form, borrowers can initiate a smoother transition away from their mortgage obligations while providing lenders with a quicker path to recover their investment. The Deed in Lieu of Foreclosure form outlines essential details, including the property description, the parties involved, and any existing liens or encumbrances. Additionally, it typically includes provisions that address the borrower's rights and responsibilities throughout the process. Understanding this form is crucial for homeowners looking to make informed decisions in challenging financial times, as it can significantly influence their next steps and overall financial health.

After completing the Georgia Deed in Lieu of Foreclosure form, the next step is to submit it to the appropriate parties. This typically involves sending the signed document to your lender and possibly recording it with the county clerk's office. Ensure you keep copies for your records.

Understanding the Georgia Deed in Lieu of Foreclosure form can be tricky. Here are nine common misconceptions about this legal document:

Being informed about these misconceptions can help homeowners make better decisions regarding their financial situation and property options.

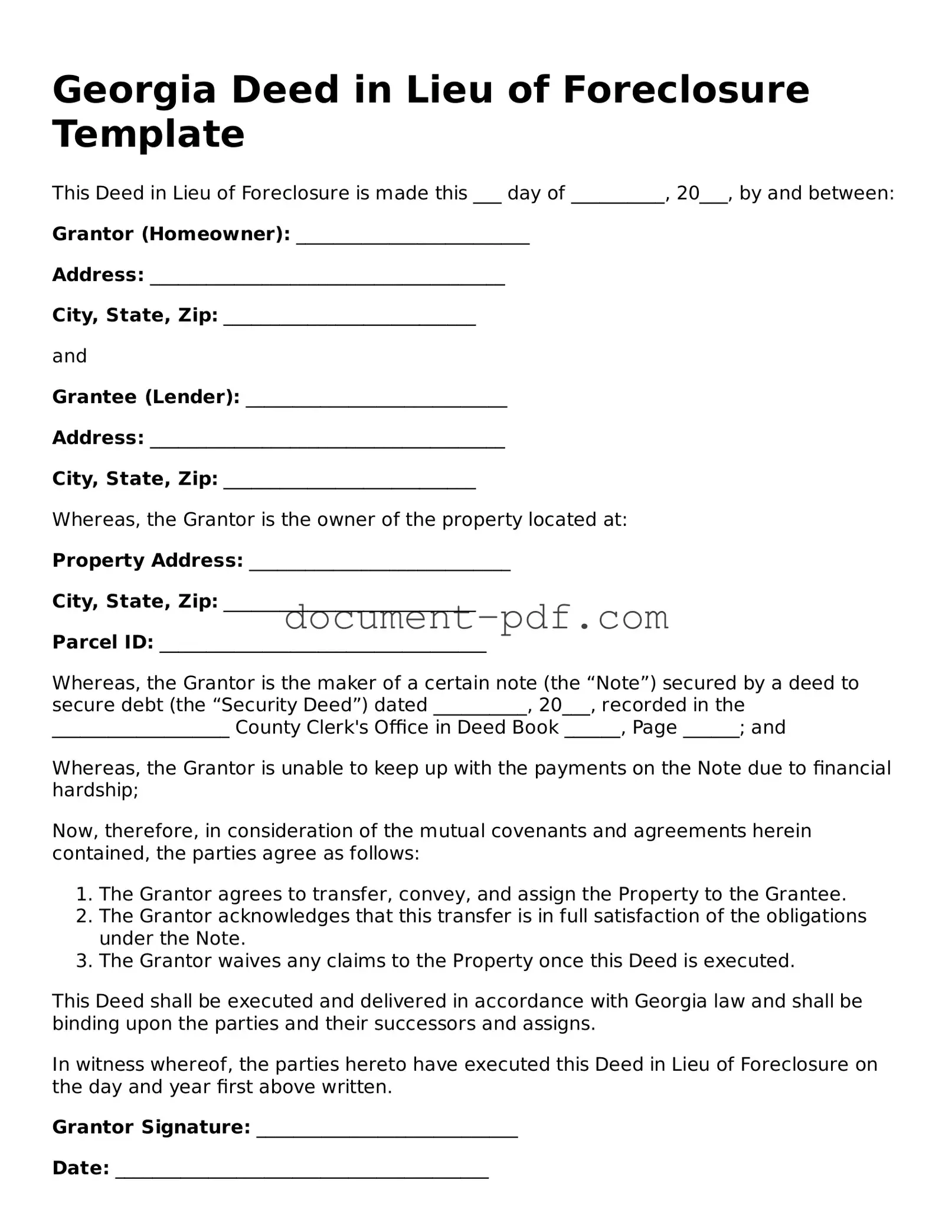

Georgia Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure is made this ___ day of __________, 20___, by and between:

Grantor (Homeowner): _________________________

Address: ______________________________________

City, State, Zip: ___________________________

and

Grantee (Lender): ____________________________

Address: ______________________________________

City, State, Zip: ___________________________

Whereas, the Grantor is the owner of the property located at:

Property Address: ____________________________

City, State, Zip: ___________________________

Parcel ID: ___________________________________

Whereas, the Grantor is the maker of a certain note (the “Note”) secured by a deed to secure debt (the “Security Deed”) dated __________, 20___, recorded in the ___________________ County Clerk's Office in Deed Book ______, Page ______; and

Whereas, the Grantor is unable to keep up with the payments on the Note due to financial hardship;

Now, therefore, in consideration of the mutual covenants and agreements herein contained, the parties agree as follows:

This Deed shall be executed and delivered in accordance with Georgia law and shall be binding upon the parties and their successors and assigns.

In witness whereof, the parties hereto have executed this Deed in Lieu of Foreclosure on the day and year first above written.

Grantor Signature: ____________________________

Date: ________________________________________

Grantee Signature: ____________________________

Date: ________________________________________

This document may not cover all aspects of the Deed in Lieu of Foreclosure process. Consulting with a legal professional is advised to ensure compliance with all local and federal laws.

When considering a Deed in Lieu of Foreclosure in Georgia, it’s essential to understand the implications and processes involved. Here are six key takeaways to keep in mind:

Understanding these key aspects can empower homeowners facing financial difficulties to make informed decisions about their property and financial future.

California Pre-foreclosure Property Transfer - It presents a straightforward solution for both lenders and borrowers facing mortgage challenges.

Deed in Lieu of Mortgage - Can improve the chances of a smooth property transition for all involved.

The Texas Notice to Quit form is a legal document used by landlords to inform tenants of their intention to terminate a rental agreement. This notice provides the tenant with a specified timeframe to vacate the premises. For templates and further information, one can visit texasformsonline.com/free-notice-to-quit-template/. Understanding this form is essential for both landlords and tenants to ensure compliance with Texas rental laws.

Deed in Lieu of Foreclosure Sample - A method to clear up outstanding mortgage debt through property transfer.

Deed in Lieu Vs Foreclosure - It's important to note that lenders must agree to this arrangement before it can be finalized.

When filling out the Georgia Deed in Lieu of Foreclosure form, it is crucial to approach the process with care. Here are five essential dos and don'ts to guide you:

By following these guidelines, you can help ensure that the process goes smoothly and that your rights are protected.

A mortgage release is a document that signifies the end of a mortgage agreement. Similar to a deed in lieu of foreclosure, it allows a homeowner to relinquish their property to the lender. However, a mortgage release typically occurs when the homeowner has paid off their mortgage entirely, whereas a deed in lieu of foreclosure is used when the homeowner is unable to continue making payments. Both documents serve to clear the homeowner's financial obligations regarding the property, but they arise from different circumstances.

Understanding the nuances of property transfer documents can be complex, especially when considering options like the quitclaim deed or short sale agreement, but for members of the NYCERS system, it's equally important to navigate retirement options, such as the New York PDF Docs that provide necessary forms and guidelines for the F170. Completing this form accurately is vital for securing retirement benefits, similar to how property documents protect ownership rights.

A short sale agreement is another document that shares similarities with a deed in lieu of foreclosure. In a short sale, a homeowner sells their property for less than the amount owed on the mortgage, with the lender's approval. Like a deed in lieu, a short sale helps the homeowner avoid foreclosure and can provide a more graceful exit from a financial burden. Both options require lender consent and aim to mitigate losses for the lender while providing some relief to the homeowner.

A loan modification agreement is a document that alters the terms of an existing mortgage to make payments more manageable for the homeowner. While it does not involve transferring ownership of the property, it serves a similar purpose to a deed in lieu of foreclosure by helping the homeowner avoid default. Both processes aim to keep the homeowner in their home while addressing financial difficulties, but a loan modification seeks to maintain the original agreement rather than relinquishing the property.

A bankruptcy filing can also be compared to a deed in lieu of foreclosure. When a homeowner files for bankruptcy, they can potentially discharge debts, including mortgage obligations. This process may lead to the surrender of the property, similar to a deed in lieu. However, bankruptcy has broader implications for the homeowner's financial situation and credit report, while a deed in lieu focuses specifically on the property in question.

A quitclaim deed is a legal document that allows a property owner to transfer their interest in a property to another party without guaranteeing that the title is clear. While a quitclaim deed is often used for family transfers or to remove a co-owner, it can resemble a deed in lieu of foreclosure in that it involves the transfer of property ownership. However, a quitclaim deed does not necessarily involve financial distress or lender approval, making it a more straightforward process.

An assumption agreement is a document that allows a buyer to take over the seller's mortgage obligations. This is similar to a deed in lieu of foreclosure because it can provide a solution for homeowners facing financial difficulties. In both cases, the original borrower may no longer be responsible for the mortgage payments. However, an assumption agreement typically involves a buyer who is willing to take on the mortgage, while a deed in lieu involves the homeowner voluntarily giving up the property to the lender.

Finally, a foreclosure notice is a document that formally initiates the foreclosure process. It informs the homeowner that the lender intends to reclaim the property due to missed payments. While a deed in lieu of foreclosure serves as a proactive solution to avoid the negative consequences of foreclosure, a foreclosure notice represents the beginning of that challenging process. Both documents relate to the homeowner's financial struggles, but they differ significantly in their implications and outcomes.