Blank Mortgage Statement PDF Form

Documents PDF

Blank Mortgage Statement PDF Form

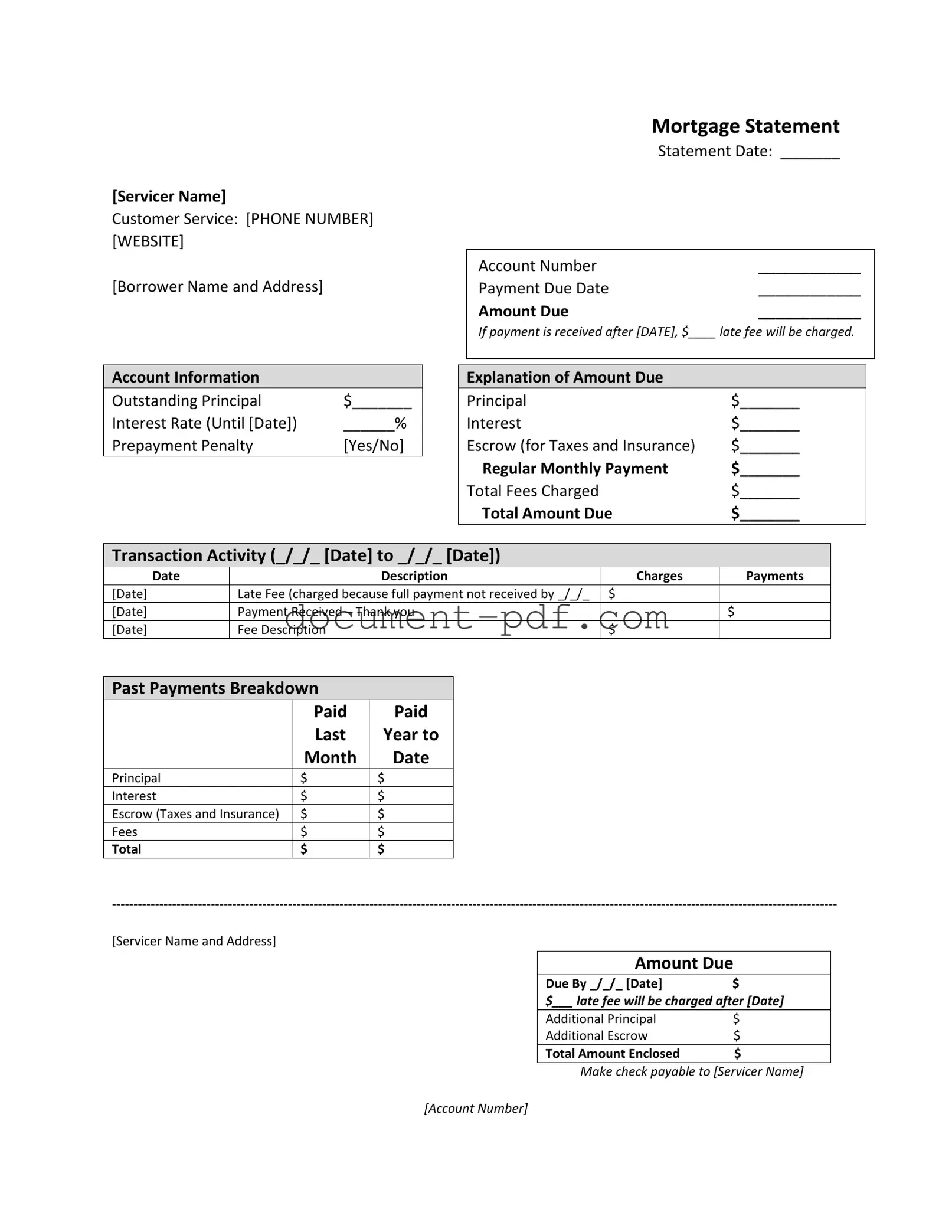

The Mortgage Statement form serves as a crucial document for homeowners, providing essential information about their mortgage account. This form includes the servicer's name and contact details, ensuring borrowers know where to seek assistance. It lists the borrower's name and address, along with key dates such as the statement date and payment due date. The form specifies the amount due and highlights any potential late fees if payments are not made on time. Account information is detailed, revealing the outstanding principal, interest rate, and whether a prepayment penalty applies. A breakdown of the amount due is provided, showing the principal, interest, escrow for taxes and insurance, and total fees charged. Transaction activity is documented, illustrating recent charges and payments, including any late fees incurred. Additionally, the form contains a section for past payments, allowing borrowers to track their payment history over the last year. Important messages address partial payments and the consequences of delinquency, emphasizing the need for timely payments to avoid foreclosure. For those facing financial difficulties, the form offers resources for mortgage counseling, ensuring that borrowers are informed of their options.

After obtaining the Mortgage Statement form, you will need to fill it out with the necessary information. This process involves entering your personal details, account information, and payment history. Ensure all information is accurate to avoid any issues with your mortgage account.

Once you have filled out the form, review all entries for accuracy. This ensures that your payment is processed correctly. If you have any questions about the form or your mortgage, contact customer service for assistance.

Understanding your mortgage statement is crucial for managing your home loan effectively. However, there are several misconceptions that can lead to confusion. Here are four common myths about mortgage statements:

Being aware of these misconceptions can help you navigate your mortgage statement with confidence and avoid potential pitfalls.

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.

When filling out and using the Mortgage Statement form, it’s essential to understand the key components to manage your mortgage effectively. Here are some important takeaways:

By keeping these takeaways in mind, you can better navigate your mortgage statement and maintain a clear understanding of your financial responsibilities.

96 Well Plate Diameter - Commonly used for assays in molecular biology and biochemistry.

To protect your family's future, consider preparing a professional Last Will and Testament that outlines your wishes clearly. This document plays a crucial role in ensuring your assets are distributed according to your desires. For guidance on how to create this important legal document, visit the page on Georgia's free Last Will and Testament resources.

Fed Ex Delivery Manager - This form must be printed and signed before affixing it to the designated delivery location.

When filling out the Mortgage Statement form, it is essential to ensure accuracy and clarity. Here are eight important do's and don'ts to consider:

By following these guidelines, you can navigate the Mortgage Statement form with confidence and clarity.

The first document similar to a Mortgage Statement is a Billing Statement. Like a Mortgage Statement, a Billing Statement outlines the amounts owed, due dates, and payment history. It provides a clear breakdown of charges, including principal and interest, making it easy for borrowers to understand their financial obligations. Both documents serve as reminders for upcoming payments and include information about late fees, ensuring that borrowers are aware of potential penalties for late payments.

Another related document is the Loan Statement. This document summarizes the details of a loan, including the outstanding balance, interest rate, and payment history. Similar to the Mortgage Statement, a Loan Statement provides a snapshot of the borrower’s financial status with respect to the loan. It also includes information about any fees charged and the total amount due, helping borrowers keep track of their payments and any changes in their loan terms.

A Payment History Report is also akin to a Mortgage Statement. This report details all payments made on the mortgage, including dates, amounts, and any outstanding balances. While the Mortgage Statement may present this information in a more condensed format, the Payment History Report offers a comprehensive view of the borrower’s payment behavior over time. This can be particularly useful for borrowers looking to understand their payment patterns and any potential areas for improvement.

In addition to these documents, those involved in buying or selling motorcycles in Texas should also be familiar with the importance of a Motorcycle Bill of Sale. This form, which you can find through Texas PDF Templates, is essential as it not only records the transfer of ownership but also serves as legal evidence of the sale, ensuring both parties have a clear understanding of the transaction details.

Next, a Statement of Account is comparable to a Mortgage Statement in that it provides a detailed account of all transactions related to a specific account. This document includes not only the current balance and payment due but also a history of all charges and payments made. Both documents aim to keep the borrower informed about their financial standing and any obligations they have, making it easier to manage payments effectively.

Lastly, an Escrow Statement shares similarities with a Mortgage Statement, particularly in the way it details escrow account activity. Both documents inform borrowers about the funds set aside for property taxes and insurance. The Escrow Statement breaks down the amounts collected and disbursed from the escrow account, while the Mortgage Statement includes escrow as part of the total monthly payment. This helps borrowers understand how their payments contribute to their overall financial responsibilities related to homeownership.