Attorney-Approved Promissory Note Document

Documents PDF

Attorney-Approved Promissory Note Document

A Promissory Note is an essential financial document that outlines a borrower's promise to repay a specific amount of money to a lender under agreed-upon terms. This form plays a critical role in personal and business transactions, serving as a legally binding agreement that details the loan amount, interest rate, repayment schedule, and maturity date. It ensures that both parties understand their rights and obligations, fostering transparency and trust. In addition, the Promissory Note may include provisions for late fees, prepayment options, and consequences for defaulting on the loan. By clearly outlining these aspects, the form helps to protect both the lender's investment and the borrower's interests, making it a vital tool in financial dealings.

Once you have the Promissory Note form in hand, you’re ready to start filling it out. This form is essential for establishing the terms of a loan agreement. Follow these steps carefully to ensure all necessary information is accurately provided.

After completing the form, keep a copy for your records. It’s advisable to review the terms with both parties to ensure clarity and agreement before finalizing the document.

Understanding a Promissory Note is essential for anyone involved in lending or borrowing money. However, several misconceptions can cloud this important financial document. Below are six common misconceptions, along with clarifications to help you grasp the true nature of a Promissory Note.

By understanding these misconceptions, you can approach Promissory Notes with greater clarity and confidence. Whether you are lending or borrowing, knowing the facts can help you navigate your financial agreements more effectively.

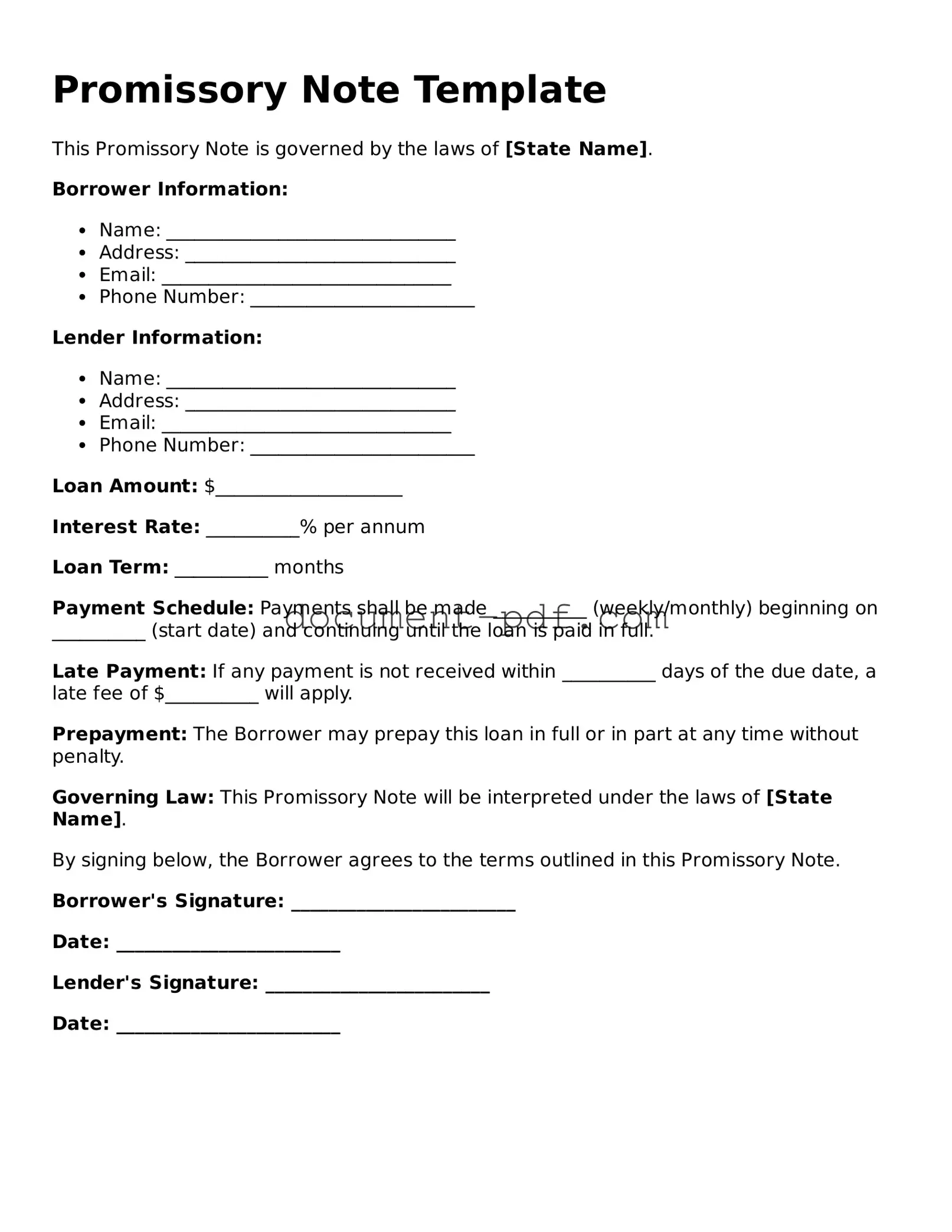

Promissory Note Template

This Promissory Note is governed by the laws of [State Name].

Borrower Information:

Lender Information:

Loan Amount: $____________________

Interest Rate: __________% per annum

Loan Term: __________ months

Payment Schedule: Payments shall be made __________ (weekly/monthly) beginning on __________ (start date) and continuing until the loan is paid in full.

Late Payment: If any payment is not received within __________ days of the due date, a late fee of $__________ will apply.

Prepayment: The Borrower may prepay this loan in full or in part at any time without penalty.

Governing Law: This Promissory Note will be interpreted under the laws of [State Name].

By signing below, the Borrower agrees to the terms outlined in this Promissory Note.

Borrower's Signature: ________________________

Date: ________________________

Lender's Signature: ________________________

Date: ________________________

Filling out and using a Promissory Note form is a straightforward process, but it is important to understand the key aspects involved. Here are some essential takeaways to consider:

Letter of Interest for Grant - Identify what makes your project stand out from others.

When considering the advantages of a Durable Power of Attorney, it is crucial to explore reliable resources for obtaining the necessary forms, such as those provided by Texas PDF Templates, which offer user-friendly options to help individuals designate their agents effectively and ensure their wishes are respected in times of need.

Home Daycare Child Care Receipt Template - Fill out the name of the child(ren) to personalize your receipt.

Submissive Kink List - Consent can be revoked at any time.

When filling out a Promissory Note form, it’s important to get it right. This document serves as a promise to pay back a loan under specific terms. Here are some essential dos and don'ts to keep in mind:

By following these guidelines, you can ensure that your Promissory Note is clear, concise, and legally sound. Happy borrowing!

A loan agreement is a document that outlines the terms and conditions of a loan between a lender and a borrower. Like a promissory note, it specifies the amount borrowed, the interest rate, and the repayment schedule. However, a loan agreement often includes more detailed provisions regarding collateral, default consequences, and other legal obligations. This makes it a more comprehensive document for larger loans or complex arrangements.

A mortgage is a specific type of loan agreement used to secure a loan for purchasing real estate. Similar to a promissory note, it requires the borrower to repay the loan amount with interest. However, a mortgage also involves the property itself as collateral. If the borrower defaults, the lender has the right to foreclose on the property, which adds a layer of complexity not found in a standard promissory note.

For those looking to navigate the intricacies of financial agreements, it is essential to understand various documentation types including promissory notes. Whether dealing with a loan, mortgage, or lease, clearly defined terms assist in maintaining transparency between parties. Additionally, resources like the pdfdocshub.com can provide valuable information regarding related forms and documents necessary for secure transactions.

A credit agreement is another document that outlines the terms of a credit arrangement between a lender and a borrower. It shares similarities with a promissory note in that it details the loan amount, interest rate, and repayment terms. However, credit agreements typically cover revolving credit lines, such as credit cards, where the borrower can draw on the credit limit repeatedly, unlike the fixed amount of a promissory note.

An IOU, or informal acknowledgment of debt, serves as a simple way for one party to recognize that they owe money to another. While it is less formal than a promissory note, it shares the fundamental concept of documenting a debt. An IOU may not include specific terms like interest rates or repayment schedules, making it less binding and more casual.

A lease agreement is similar to a promissory note in that it often involves regular payments over time, typically for renting property. Both documents outline payment terms, including the amount and frequency of payments. However, a lease agreement also includes additional details regarding the use of the property, responsibilities of both parties, and terms for termination, which are not typically found in a promissory note.

A personal guarantee is a document in which an individual agrees to be responsible for the debt of another party. It shares similarities with a promissory note in that it establishes a financial obligation. However, a personal guarantee usually serves as a secondary assurance for the lender, ensuring that if the primary borrower defaults, the guarantor will repay the debt.

A bond is a financial instrument that represents a loan made by an investor to a borrower, typically a corporation or government. Like a promissory note, a bond involves the borrowing of money with a promise to repay it, along with interest. However, bonds are generally issued in larger amounts and can be traded in secondary markets, making them more complex than a simple promissory note.

A letter of credit is a document issued by a financial institution guaranteeing payment to a seller on behalf of a buyer, provided certain conditions are met. While it serves a different purpose than a promissory note, both documents involve financial commitments. A letter of credit is often used in international trade, providing assurance to sellers that they will receive payment, similar to how a promissory note assures lenders of repayment from borrowers.